In this article

- The spending habits Brits are most likely to hide from their partner

- The impact of the cost of living crisis on romantic relationships

- Cities experiencing the most relationship strain from the cost of living crisis

- The benefits of discussing finances with your partner

- How can couples navigate conversations about finances and better manage their money together?

Couples' spending habits in the UK

Our research uncovers the financial topics that put the most strain on relationships

Finances are often an incredibly tricky subject to approach, and when you’re in a relationship this conversation can be even more challenging to navigate. You might be looking at moving towards combining finances, and you’ll likely have different incomes and spending habits making this a potentially strenuous process. But what are the biggest challenges couples face when it comes to money, have they changed since the start of the cost of living crisis and more importantly, how can we look to solve them?

We recently conducted a survey of 1,239 UK residents currently in a relationship to discover what their most significant financial challenges are, and how the cost of living crisis has impacted their relationships. 31% admitted to arguing with their partner about finances, which increases to 46% for those aged 16-24. With all these issues that couples are facing, what can couples do to help remove money as a friction point in their relationship?

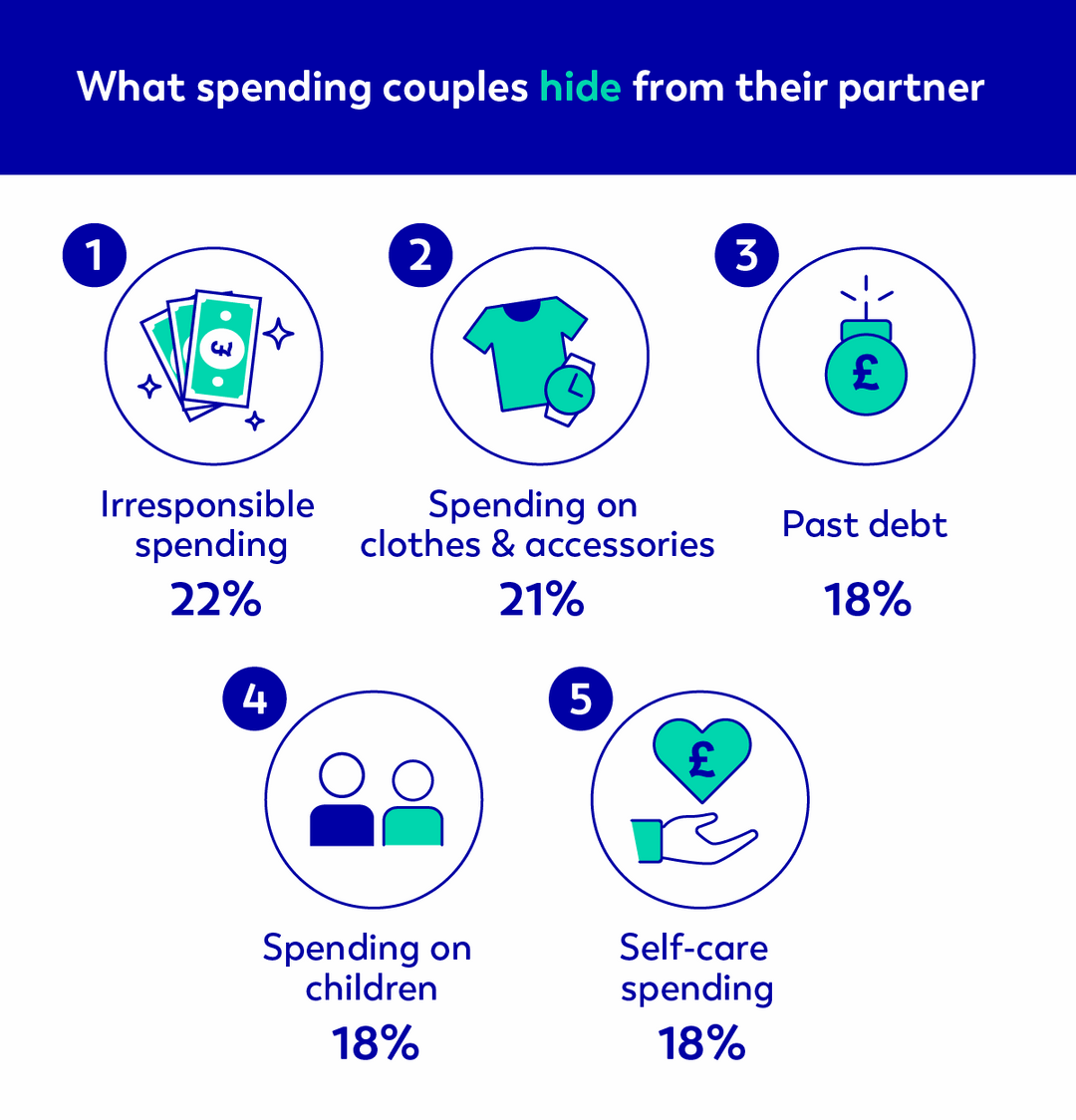

The spending habits Brits are most likely to hide from their partner

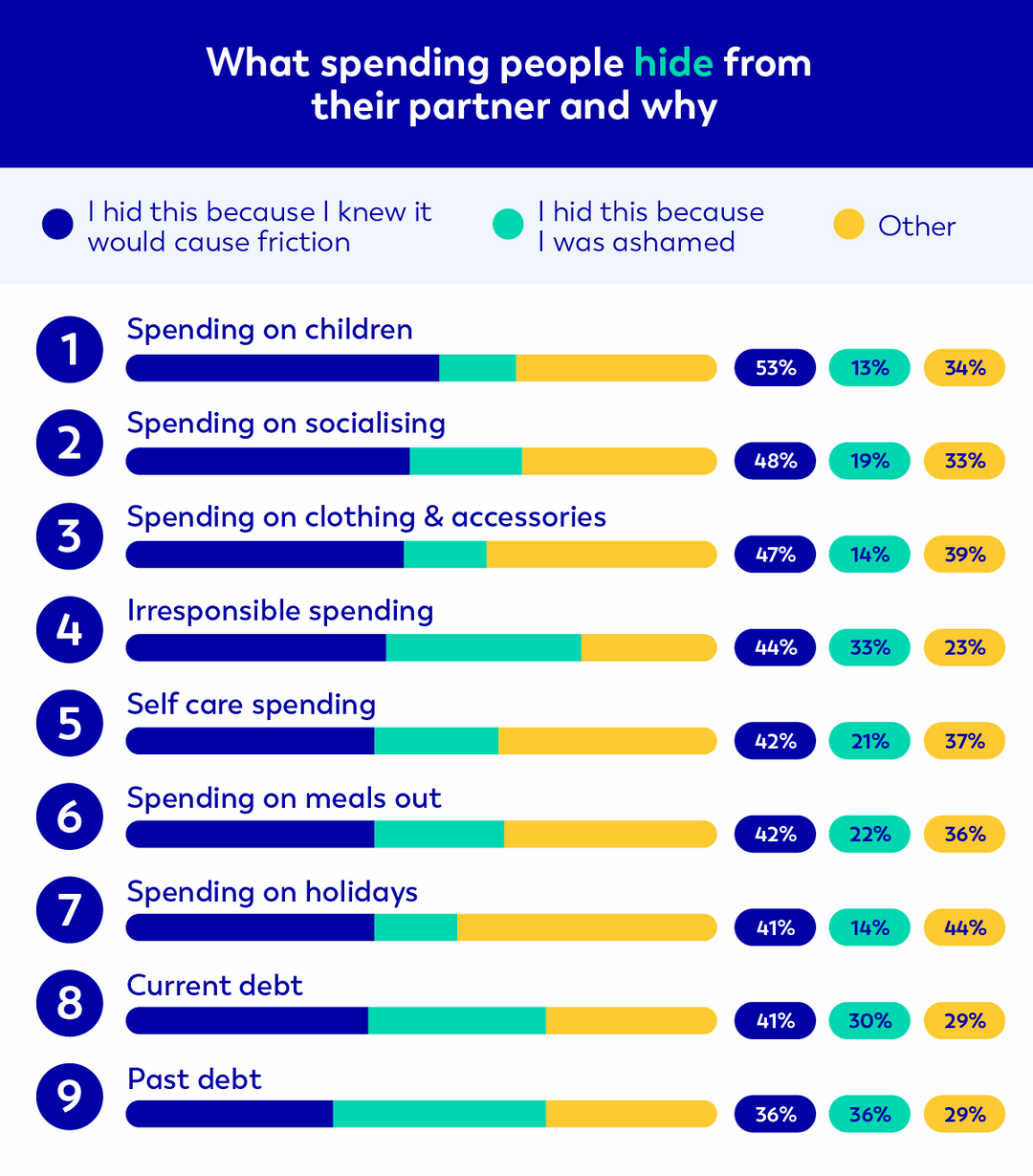

Since many financial topics are sensitive to discuss, a lot of couples will avoid talking about them altogether. Our survey found that over a fifth (22%) of Brits admit to hiding irresponsible spending from their partner; 21% admit to hiding how much they spent on clothing and accessories; and 18% admit to hiding self-care spending, past debt and how much they spend on their children.

We also found that while women are most likely to hide how much they spend on clothes and accessories - 24% compared to 18% of men - men are most likely to hide how much they spend on socialising, with 20% of men hiding this compared to only 13% of women.

Additionally, our study revealed that the motivating factor behind people hiding different financial habits from their partners was knowing it would cause friction between them.

The impact of the cost of living crisis on romantic relationships

We’ve all seen the effect that the cost of living crisis has had on our finances, but it has also taken its toll on our relationships. As many as 35% of UK couples have admitted to the cost of living crisis causing a strain on their relationship, and 28% of respondents said that it has led to them arguing about finances more frequently.

Our survey revealed that debating how to change spending habits due to the cost of living crisis is the most sensitive financial topic for couples, with 37% of respondents agreeing that this is a difficult topic. This is followed by addressing a partner’s excessive spending from their personal account (29%), and how much a partner wants to spend on everyday items (29%).

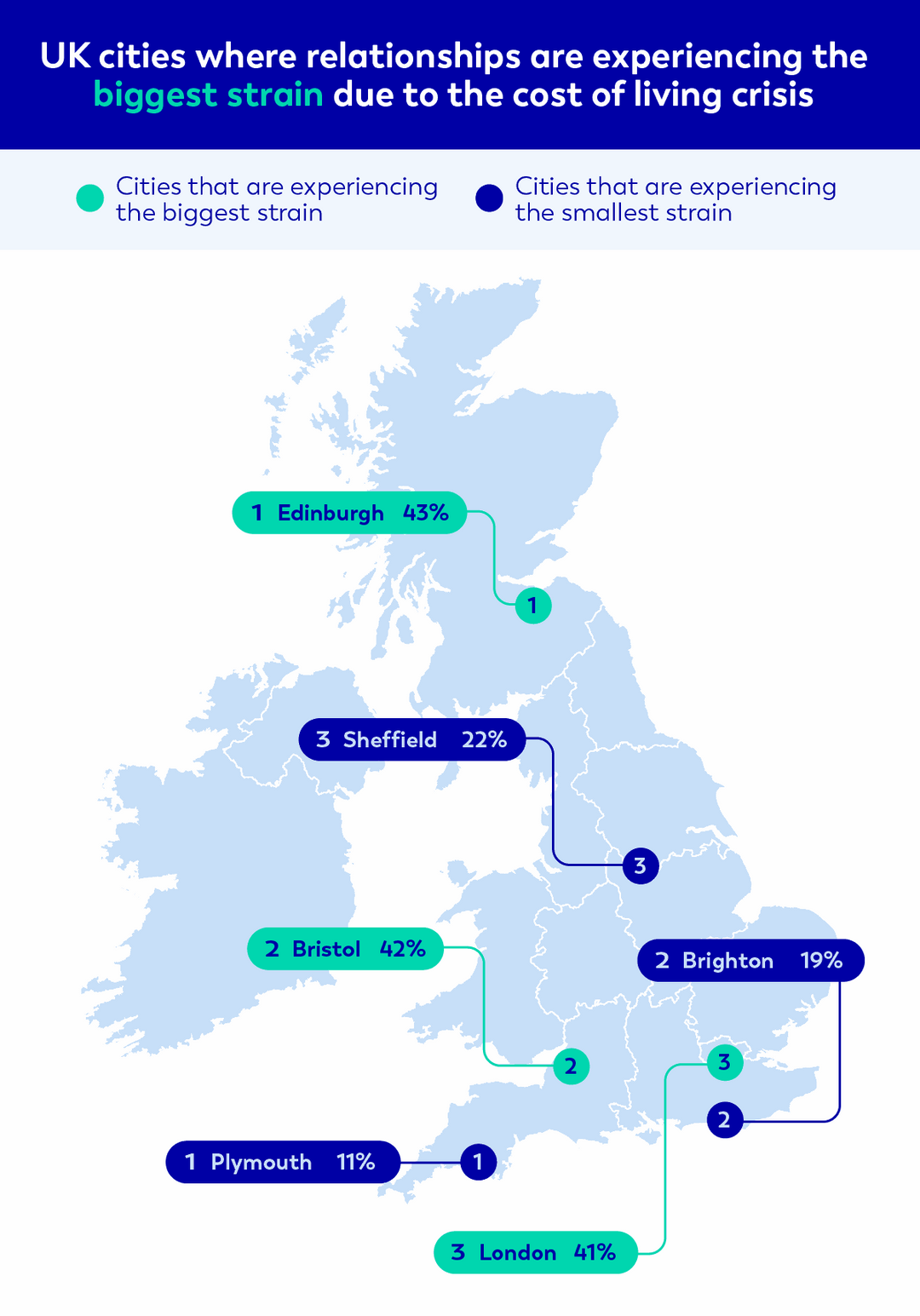

Cities experiencing the most relationship strain from the cost of living crisis

Couples in Edinburgh are experiencing the most strain (43%) due to the cost of living crisis, closely followed by those in Bristol (42%) and London (41%).

Meanwhile, Plymouth residents seem to be experiencing the least strain, with only 11% of couples saying the cost of living crisis has impacted their relationship. This is followed by Brighton, where just 19% of couples say their romantic relationship has been affected.

The benefits of discussing finances with your partner

Although finances can be hard to discuss, open communication with your partner about spending can be beneficial. We found that 27% of Brits with joint finances said that it has made them more aware of what they spend their money on, and 23% said that it made them more aware of how much they spend overall.

Additionally, those aged between 16-44 said that it also makes them more motivated to save money, as they’re saving with their partner rather than alone.

How can couples navigate conversations about finances and better manage their money together?

Managing money as a couple will be different for everyone, and it seems there’s no “one-size fits all” approach. To get some tips, we spoke to relationship consultant and strategist, Mairead Molloy:

1. Consider whether you want to fully combine your finances

“There are some good reasons not to combine, or at least not fully combine finances. If one of you has significant savings or significant debts, it could very well be worth it to not share bank accounts. If you divorce and your savings are in a joint account, your spouse could get half of them. What you could do is keep your own account - but open a joint account for household bills and special projects, such as holidays, house renovations, etc.”

2. Always have your own account

“It’s absolutely critical, especially for women, that you keep money in an account that’s yours that you control. Nearly 50% of marriages end and often the woman sees the biggest impact financially in divorce. So it’s good to have your own investment account, your own emergency account, and your own credit score.”

3. Create a budget depending on earning capacity

“You can keep a joint account, or a 'we account', in which you can together save money for shared expenses like rent, bills, insurance, taxes and food, as well as large purchases that you’re saving for as a team.”

4. Determine what’s important to you

“It’s important to make conversations about money a standing, recurring thing. Depending on your relationship and your finances, that could be once a week, once a month, one a quarter - they can be short or long, as long as they’re regular. Determine the parts of your finances that are important to you and keep an eye out for any financial red flags. If you do see any, make sure to talk about them with your partner."

Mairead Molloy, relationship consultant and strategist, comments:

“Whether you're in a brand new relationship or you've been committed for a while, take some time to sit down with your partner and talk through your feelings about money.”

“You and your partner should have equal say (and equal power) in financial decisions. Couples often seek therapy when there is an imbalance in the relationship — sometimes a partner who makes more money believes they should have more say in decisions. Other times,” she says, “the person who is more anxious or frugal about money gets more say.”

“If this imbalance isn't equalised, both couples can end up with hurt feelings. It can bring up a lot of feelings, sometimes inadequacy, resentment, sometimes a lot of feelings about dependency - talking about money can help us grow closer emotionally.”

If someone is controlling you financially, this could be domestic abuse. Visit National Domestic Abuse Helpline to spot the signs and get help.

Aqua strives to help you improve your credit no matter your financial situation. We aim to give people a chance by saying yes when other lenders would say no, and provide the right tools and support to help them on their way toward a better credit score. Since 2002, we’ve said yes to over 2 million people so they can start their journey towards better credit thanks to our credit card for bad credit.

Check out our building credit section to find helpful information on credit and learn how to actively improve your credit history.

Representative 39.9% APR variable for Aqua Classic.

Footnotes and sources: This survey was conducted across 1,239 UK residents over the age of 16 that are currently in a relationship.

Index methodology: Aqua surveyed 1,239 UK residents in August 2022.

Failure to make payments on time or to stay within your credit limit means that you will pay additional charges and may make obtaining credit in the future more expensive and difficult.

Contributors

You might also like

Slide 1 of 3

The Social Tax: UK adults overspend by £800 d...

Over a quarter of those surveyed said they overspend due to the fear of missing out.

The cost of a first date

Survey finds almost a quarter of single Brits are planning to stop dating due to the cost of living crisis.

Everyday budgeting

Budgeting bills and everyday budgeting tips.

The smart way to build better credit

Aqua is the credit card that gives you the power to improve your credit score