In this article

Financial Learnings and Mistakes 2025

New survey from Aqua reveals the UK’s biggest financial learnings and mistakes

With everyday costs on the rise, it’s more important than ever to feel confident about your finances. Yet, that’s often easier said than done.

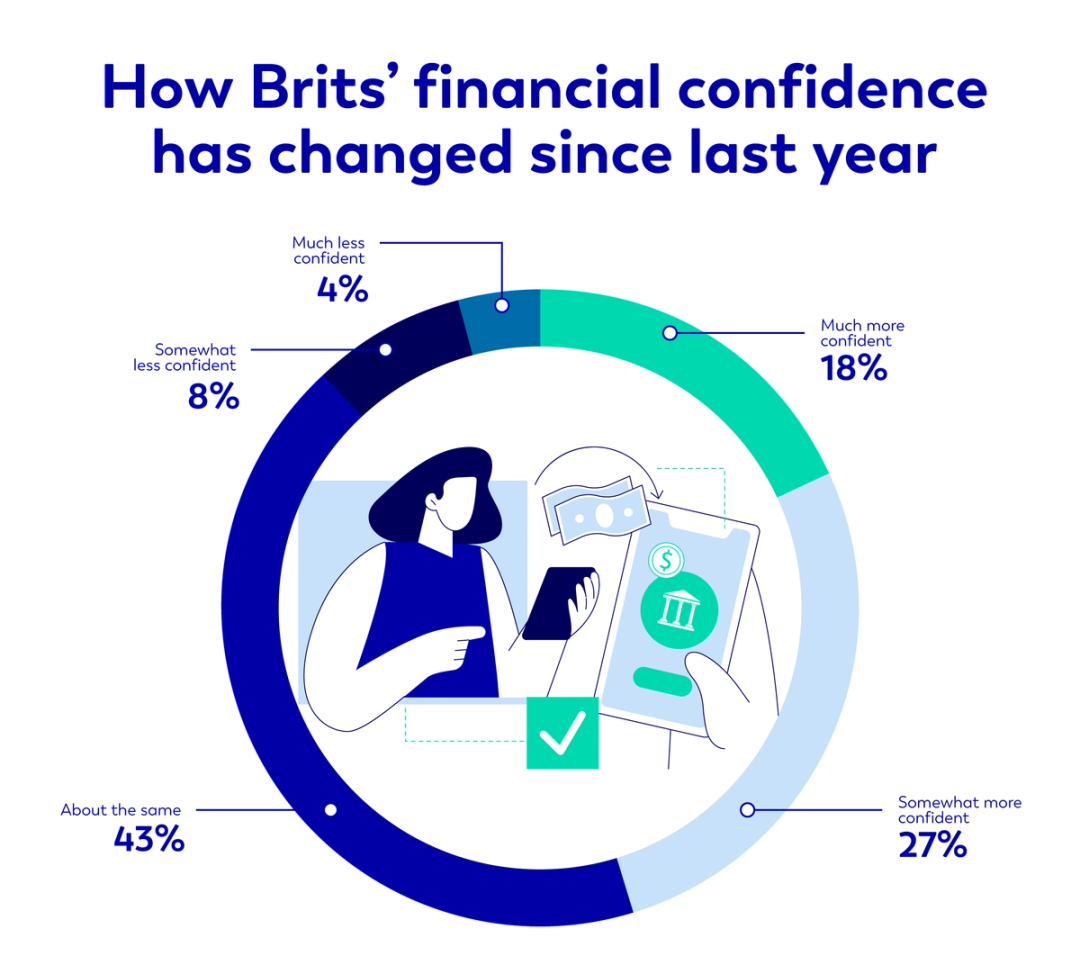

Encouragingly, nearly half of Brits (46%) now say they feel more confident about their finances than they did this time last year, a hopeful sign of resilience. However, our latest research shows that many people continue to feel the impact of poor credit, with 37% of Brits saying they currently have, or have had, a bad credit score. These findings highlight the ongoing importance of understanding credit and maintaining healthy financial habits.

To learn more, we surveyed 5,000 adults across the UK to explore the prevalence of bad credit and common financial mistakes, as well as the lessons people have learned along the way, and compared the results to our report from 2024. We’ve also included practical insights which may help you build your credit score and boost your overall financial wellbeing.

How the UK feels about their financial situation in 2025

Our latest survey shows that, even in a challenging financial climate, many people across the UK feel positive about their financial situation. The most common emotions this year are feeling ‘stable’ (20%), followed by ‘content’ (16%), and ‘happy’ (12%). In fact, these emotions have increased by a combined 10% over the last year. Those aged 55 and over feel the most financially stable, followed by individuals aged 25–34, highlighting that older adults and young professionals are currently the most confident about their finances.

However, not everyone feels as positively. Around one in ten (10%) said they feel ‘anxious’ about their current financial situation, with a further 9% stating they feel ‘stressed’. While these feelings still remain, overall, fewer people are experiencing negative emotions about their finances compared to last year.

The UK’s biggest financial mistakes

A key focus of our survey was the financial mistakes people have made. Respondents were asked to rank common financial mistakes they admitted to experiencing, based on which had the biggest impact.

Not planning for retirement is cited as the biggest financial mistake for almost half of Brits (45%), a concern most commonly reported by those aged 55 and over, while it is less of a concern for 25–34 year olds, who instead cite overspending as their biggest financial mistake, highlighting how financial priorities and pressures shift at different life stages. 40% also said accumulating debt through credit cards was their biggest financial regret. Overspending or spending beyond their means follows, cited by 38% of respondents.

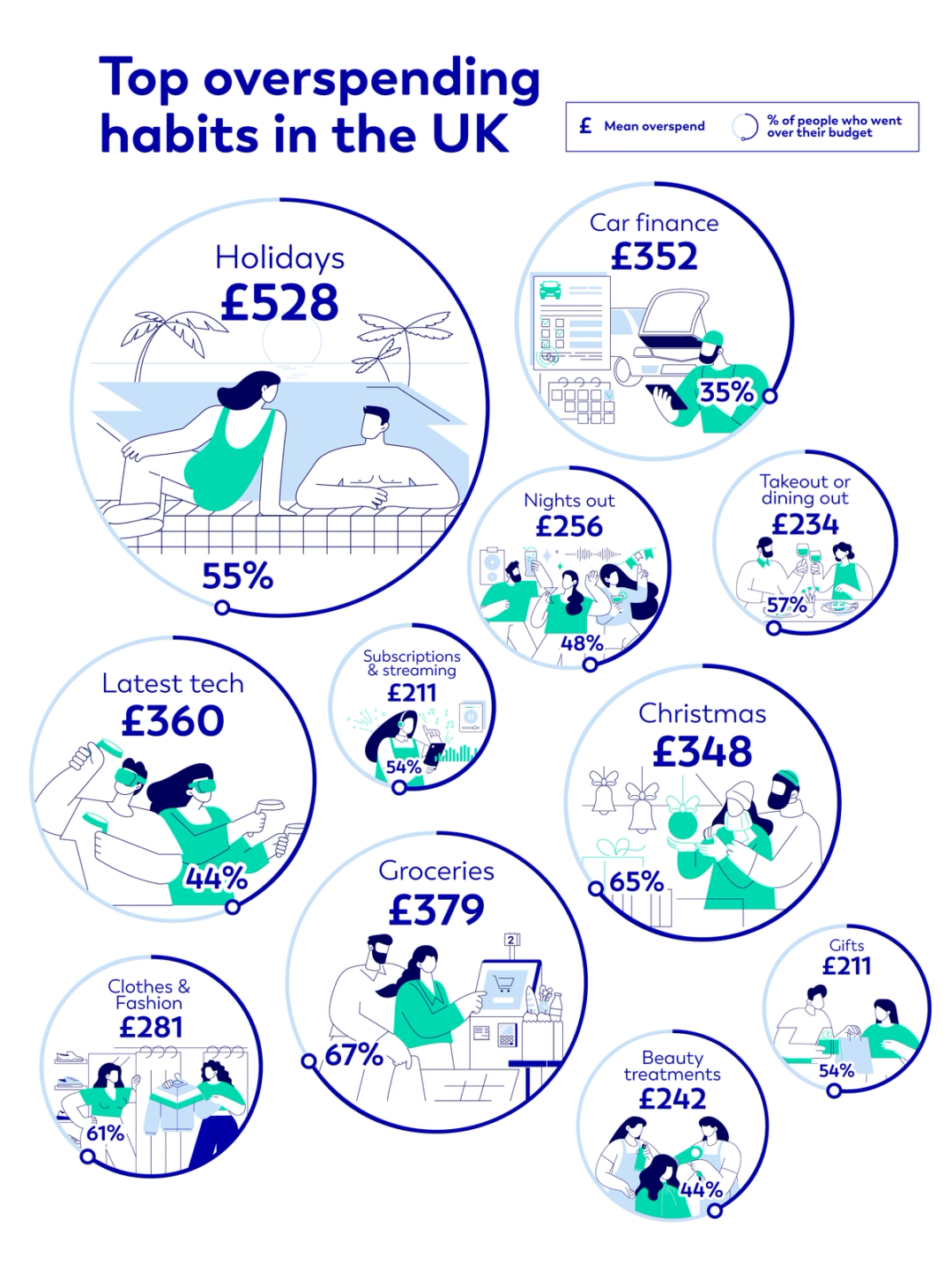

Overspending and spending outside of their means topped the list in last year's study, so this year, we wanted to dig deeper to understand just what people were overspending on.

What Brits are most likely to go over their budget for?

The struggle of creating or adhering to a budget is a recurring theme, with the average Brit confessing to overspending in a range of areas. People are most likely to overspend on their weekly food shop (67% going over budget), and almost a quarter of Brits (24%) admit they don’t set a budget for groceries at all. But in terms of actual spend, holidays are the biggest drain, with an average annual overspend of £528 (55% of people).

Other notable overspends include new technology (£360) and home improvements (£361). Christmas is an especially costly period, as Brits admit to an average festive overspend of £348 for just a couple of weeks.

The impact of financial mistakes

From overspending to making a decision that may not support your financial wellbeing, navigating your finances can be tough, and mistakes can have a significant impact on financial stability, relationships and general wellbeing. In fact, 32% of those who said they had been affected by financial challenges reported increased stress.

From a financial point of view, one in four (25%) respondents said they got into debt as a result of their financial mistakes, and 23% reported a decrease in their credit score. 16% of those surveyed reported experiencing physical symptoms, including headaches or difficulty sleeping, while just over one in 10 (11%) said their romantic relationships had been affected.

The impact of poor credit

The study revealed that almost a quarter of Brits reported a decrease in their credit score due to a previous financial mistake, so it’s important to be aware of the impact this can have across the rest of your finances, future plans, as well as your emotional wellbeing.

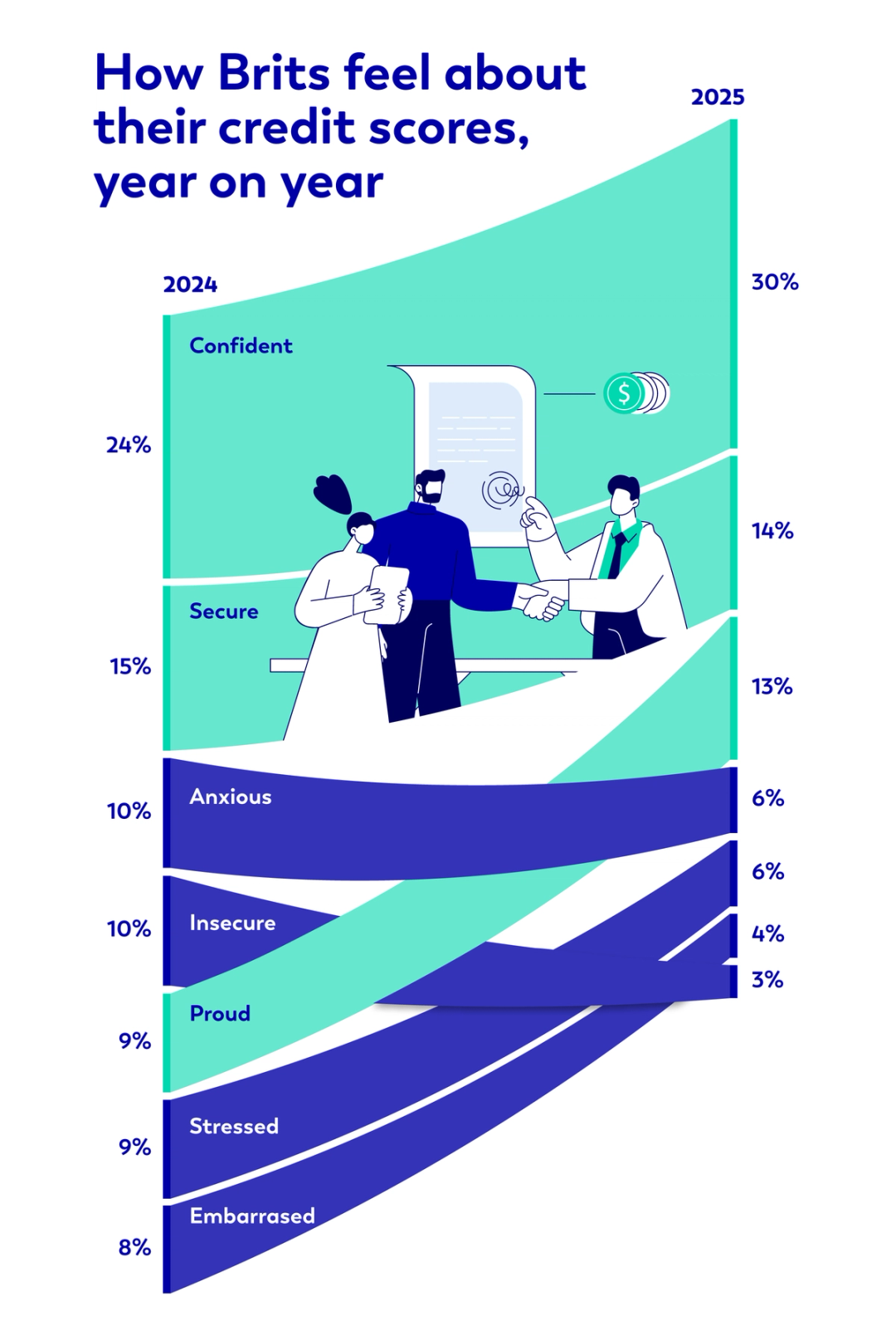

When asked what impact poor credit had on their life, some respondents stated that stress, frustration, and anxiety remain a reality. 13% of those surveyed reported they have felt stressed about their low credit score; however, this has notably halved over the last year, down from 26% in 2024.

In fact, more people are taking steps to regain control of their credit scores. Of those surveyed who answered to knowing their credit score, 53% are actively working to improve it, which is 17% more than in our 2024 survey, a very promising jump.

Confidence is also growing. 30% of respondents overall said they are confident in their credit score, while 13% described themselves as proud. Both of these responses show a significant increase from 12 months ago, when 24% of Brits said they were confident and 9% felt proud.

Bad credit can also have practical consequences - it can make it harder to access certain services that rely on financial stability. The top financial impact Brits experience due to poor credit is difficulty in getting accepted for a credit card, with one in three (33%) affected. This overtakes 2024’s most commonly mentioned issue of paying higher interest rates (24%).

Other common impacts include the inability to obtain a personal loan (27%) or access balance transfer offers (18%). 25-34 year olds are the most affected demographic in this regard, with one in four (25%) admitting to being unable to use balance transfer offers to manage their debt.

Sharvan Selvam, Commercial Director at Aqua, has shared tips on how to secure a credit card if you have low credit:

“We know how frustrating it can be when bad credit history makes it more difficult to get a credit card, in turn making it more difficult to get yourself back on track. There are, however, a few things you can do to increase your chances.”

- Get a credit-builder credit card. These have a lower qualifying threshold and a lower credit limit, enabling you to make smaller, lower-risk purchases. Paying the balance off on time will allow you to build your credit score.

- Alternatively, a secured credit card is easier to qualify for. It requires a refundable cash deposit equal to your credit limit, which you’ll get back if you close the account in good standing. Using the card responsibly can improve your chances of later qualifying for an unsecured credit card.

- Research your options - applying for credit requires a ‘hard check’ credit report review by the lender, and multiple applications in a short space of time can negatively impact your credit score. Before applying for a credit card, check your eligibility through a soft search, which doesn’t impact your credit score.

Improving your credit score to reduce stress

Our research shows that people are feeling more confident about their credit score compared to the same time last year, which begs the question: what do they wish they had done sooner?

The survey revealed that more than a quarter (28%) of Brits wish they had checked their credit score more often, and 24% wish they had started building it earlier and used credit more responsibly.

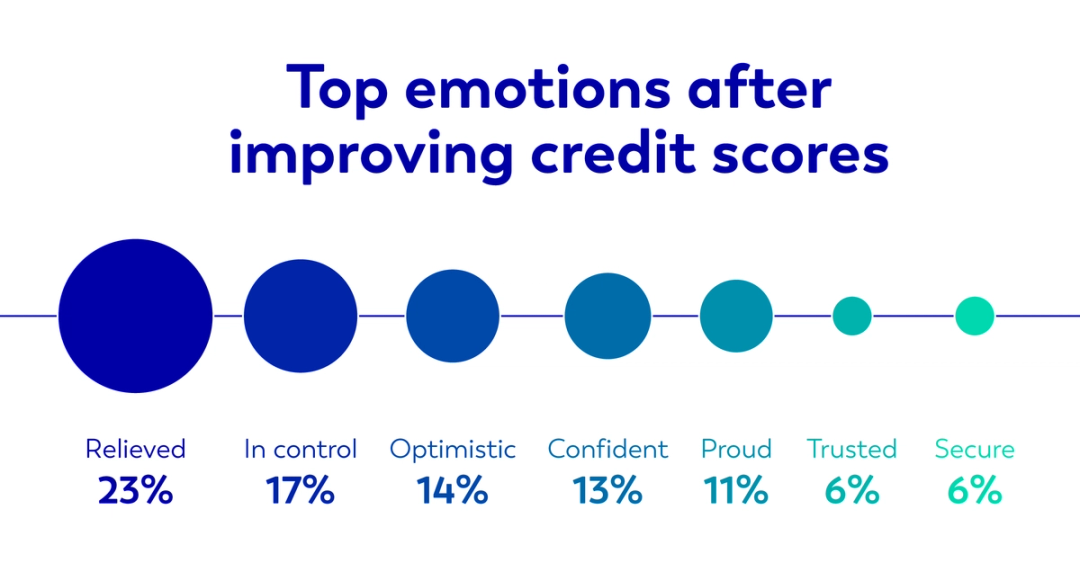

Unsurprisingly, when people improve their credit score, they feel much better. Our data shows that after boosting their score, almost a quarter (23%) of Brits felt relieved, while 17% felt more in control of their finances and 14% felt more optimistic, showing how better financial health can improve your confidence and outlook on your finances.

Sharvan says, “With more than a quarter of Brits wishing they had checked their credit score more often and just under a quarter regretting not building it earlier, the good news is it’s never too late to start.

Whilst having a bad credit score can affect many areas of your life, from being unable to take out a mortgage to not being able to take out a mobile phone contract, there are several steps you can take to start improving your credit today.

- Review your financial history: Start getting your finances in order by checking your credit report. Understanding what might be holding you back allows you to target the areas that need the most attention.

- Pay off existing debts: Lenders take your current debts into account when assessing your application, so it can help to pay down some of your current debt before seeking more credit. Consider mapping out your debts, balances, and upcoming payment dates to stay organised.

- Make your repayments on time: Demonstrating that you can consistently meet your financial commitments is key. Always pay bills and credit card balances on time and stay within your credit limits.

- Register on the electoral roll: This helps lenders verify your identity and can quickly add several points to your credit score.

- Keep old accounts active: By keeping open old accounts that are in good standing, you show lenders that you can successfully manage multiple credit accounts over a long period of time.

- Keep your credit utilisation low: Aim to use no more than around 30% of your available credit, as lenders view lower usage more favourably.

Financial learnings: what people wish they’d known sooner

Reflecting on your own financial decisions or seeing the financial mistakes others have made can offer valuable lessons. So our survey explores the biggest learnings people have taken from their own experiences, and for many, becoming more informed about their money is the first step to managing it more effectively.

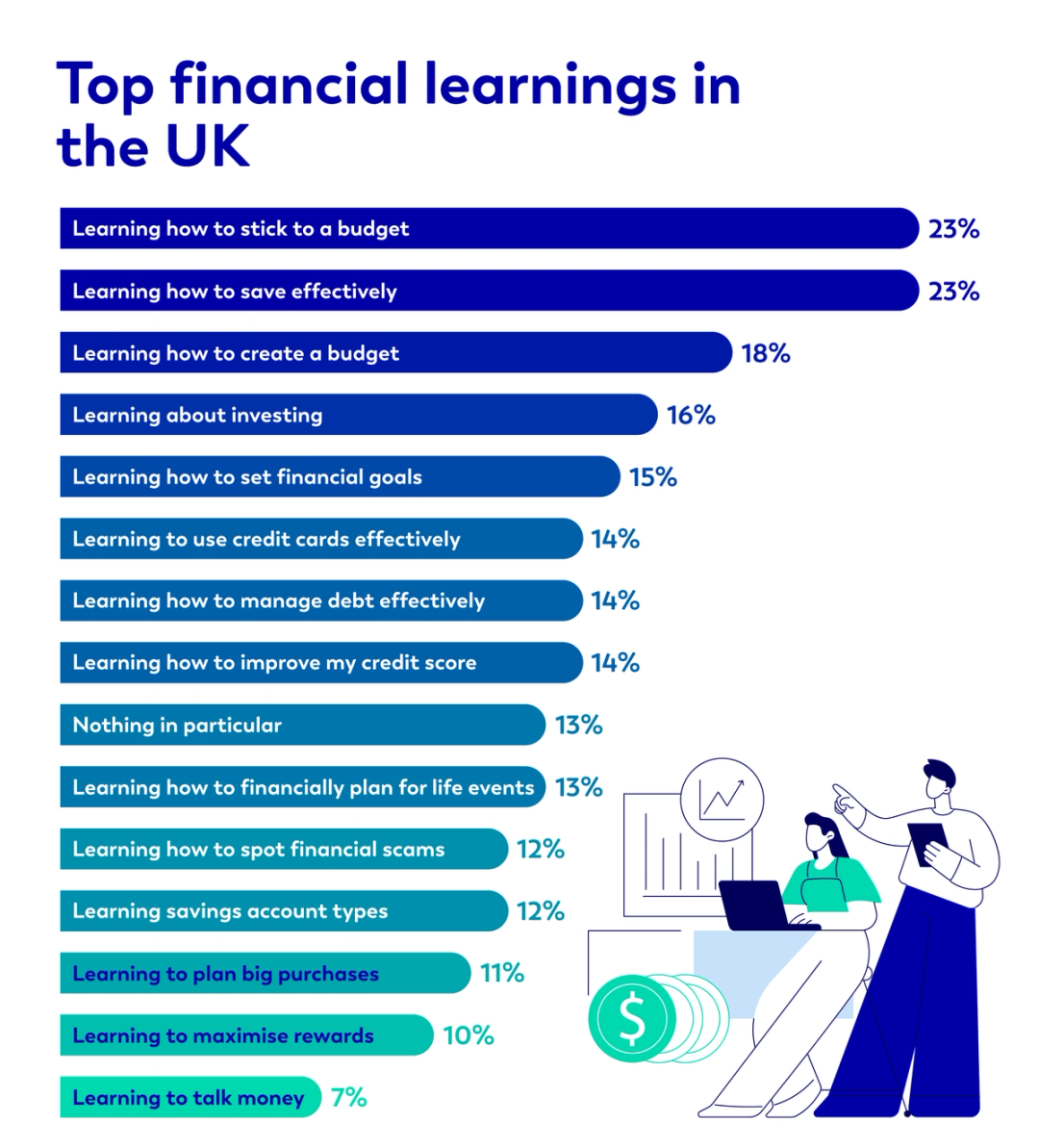

Knowing how to budget and save are the UK’s key financial learnings

Sticking to a budget and saving were joint as the biggest skills British adults have learned (23%). 18% said that learning to create a budget was one of their most important lessons, while learning about investing (16%) and setting financial goals (15%) also featured highly.

Sharvan says, “Getting started with a budget can feel daunting, but even a simple plan can make a big difference. Begin by gathering your statements and receipts to understand your current monthly outgoings. Then, compare that against your monthly income to identify areas where you could reduce non-essential spending, such as eating out. You'll then have a better understanding of how much you can save each month. The hardest part is getting started, but once you get the basics down, you'll find that managing your money is much easier and you'll feel more confident in your finances too.”

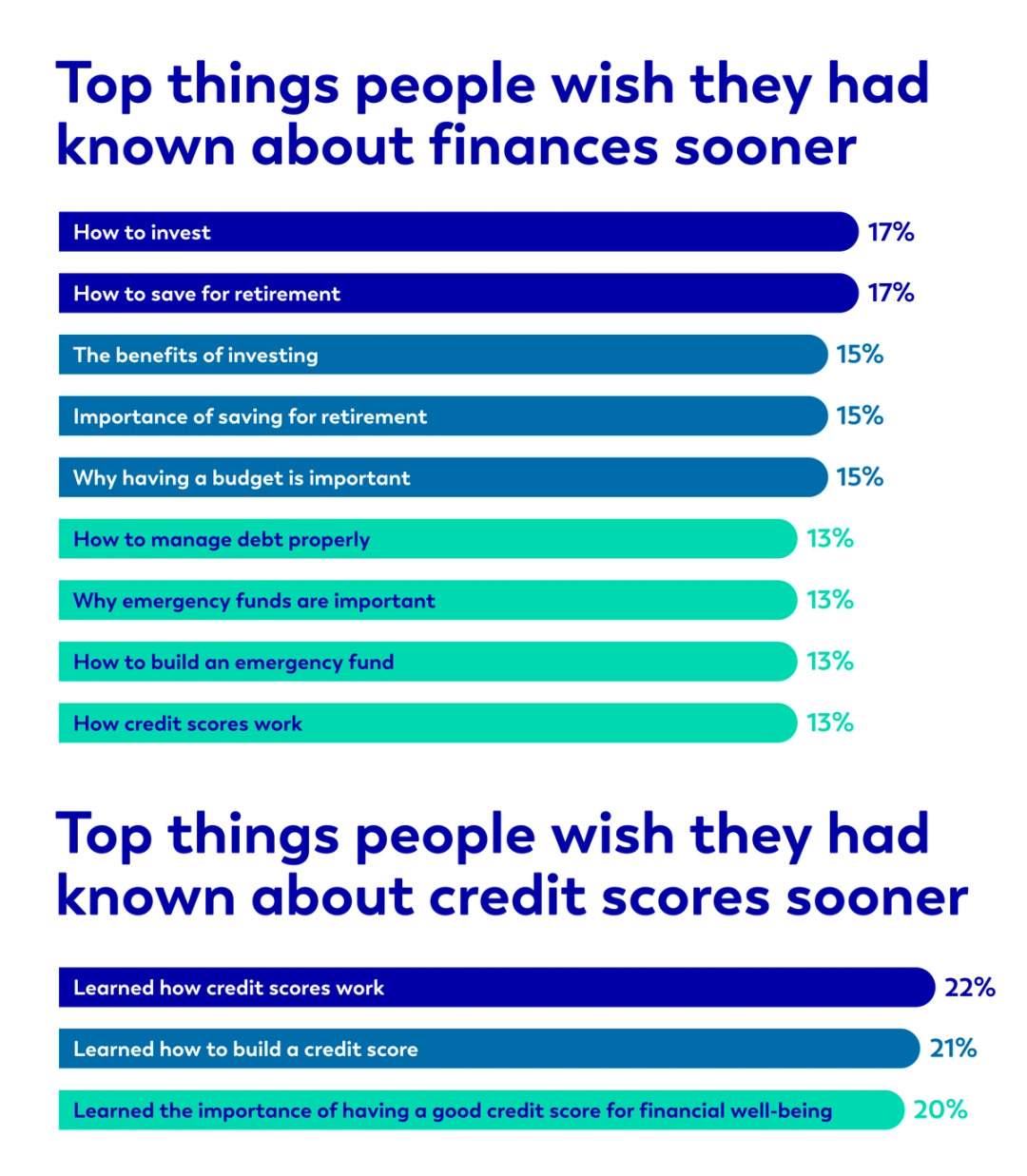

82% of UK adults wish they had learned more about their finances sooner

Financial literacy is an important element of making smart financial decisions, yet there are a number of topics that Brits wish they had learned more about, sooner. Retirement and investment-related topics top the list, both of which can be important aspects of a strong, financial future. Budgeting, debt management and the importance of emergency funds are also key areas that Brits feel could have benefited them if they had earlier knowledge.

When it comes to credit scores, 22% of people wish they had understood how they work sooner, while 21% said they wish they had known how to build their score earlier, highlighting a clear knowledge gap around credit scores.

Brits want more education, but where are they going for their financial advice?

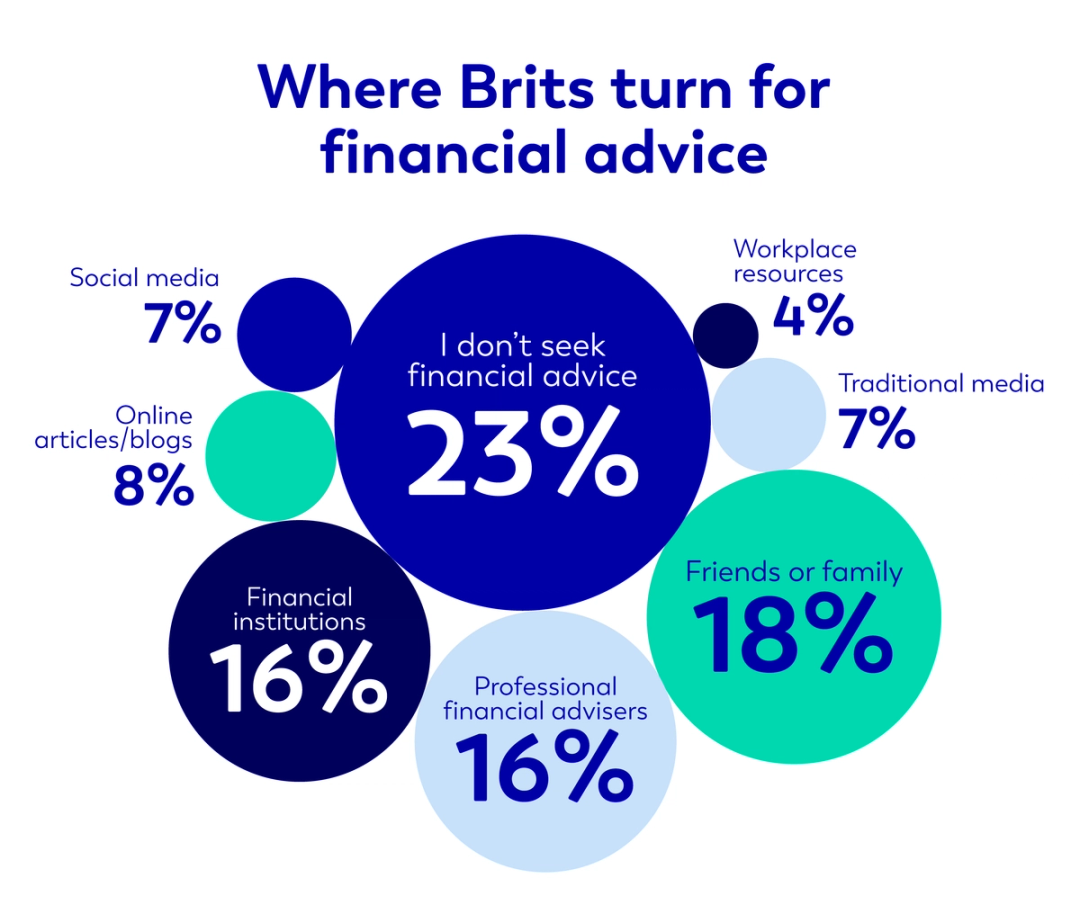

After looking at what Brits wish they had known sooner, we turned our attention to where they tend to seek financial advice to make up for the lack of earlier knowledge.

77% of people surveyed state they actively seek financial advice, with the most common source being from friends or family, cited by 18%.

Almost a quarter (22%) of 21-24 year olds said they receive financial advice from social media platforms like TikTok, although this drops sharply for older generations, with just 2% of people aged 55+ turning to these platforms.

This is a trend that is replicated with AI tools - while older generations have not yet embraced this technology (just 10% of people aged 55+), two-thirds of 25-34 year olds (67%) and more than half of 21-24 year olds (53%) use ChatGPT and similar AI tools to get financial advice.

Sharvan comments: “It’s encouraging to see so many people actively seeking financial advice, whether from professional advisers, banks, or their own networks. At the same time, the rise of social media and AI tools as a source of guidance shows how much the finance landscape is changing, particularly for younger generations.

While these platforms can provide helpful information, it’s important to check any advice given and balance it with trusted, reliable advice, especially when it comes to credit scores and long-term financial decisions. Speaking with a qualified professional remains the most reliable way to make informed choices and avoid making mistakes that could impact your financial wellbeing.”

For more advice on fixing your credit score, be sure to look at:

https://www.aquacard.co.uk/building-better-credit/how-to-fix-bad-credit-and-what-it-takes

Methodology & Sources:

This study was informed by a survey of 5,000 UK adults over the age of 21, conducted in August 2025. Responses were also filtered into various demographics to determine how different regions, genders, and age groups responded.

Failure to make payments on time or to stay within your credit limit means that you will pay additional charges and may make obtaining credit in the future more expensive and difficult.

Contributors

You might also like

Slide 1 of 3

Financial Learnings and Mistakes 2024

Aqua’s latest survey explores Brits’ biggest financial learnings and mistakes.

What is a balance transfer?

A credit card balance transfer is when you transfer the balance from one card, where you might be paying a higher a...

Financial Conversation Confidence

Aqua’s latest survey explores how Brits feel when talking about money, and why they may struggle to discuss financi...

The smart way to build better credit

Aqua is the credit card that gives you the power to improve your credit score